Corporate Social Responsibility | Digital Transformation

Written by Fanos Adams

Nov 1, 2021

Abstract/ Summary

For financial stability monitoring purposes, the supervisory authorities and regulators are continually integrating ESG risks into Capital Markets supervisory requirements. A financial sector risk assessment of potential impacts due to climate risk has become one of the major priorities for regulators. In March 2021 the European Banking Authority (EBA) published a proposal on how banks should disclose their activities in an EU-Taxonomy compliant manner. As a result, the authority requires banks to determine the Green Asset Ratio (GAR), which indicates the “green” proportion of a portfolio. The final rules are due to come into force in 2022. Banks will then be required to start with GAR related disclosures. Since the timetable is tight, banks are now encouraged to take action and to start their preparations in order to integrate the taxonomy-compliant information into their system & data infrastructure. Quantitative indicators like the GAR capture both risk and opportunities, and allow for a comparison between portfolios. Therefore, banks are advised to participate in supervisory driven pilot exercises since this is expected to give them a competitive advantage. In addition, it will help them to influence the final outcome.

1. Introduction

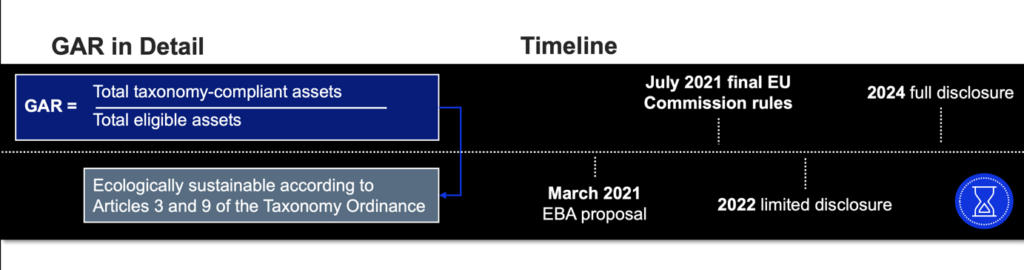

The EU Commission mandated EBA to identify Key Performance Indicators (KPIs) and methodologies for the disclosure of taxonomy-compliant activities to be used by those banks subject to the EU Non-Financial Reporting Directive (NFRD). These are all EU credit institutions, insurers and non-financial companies with more than 500 employees and listed securities on a regulated market of an EU member state. What followed is a proposal by the EBA in March 2021, according to which banks and investment firms are to determine and disclose (among other things) the “Green Asset Ratio” (GAR) in future[1]. The GAR is part of the so-called “Green Deal” of the EU.

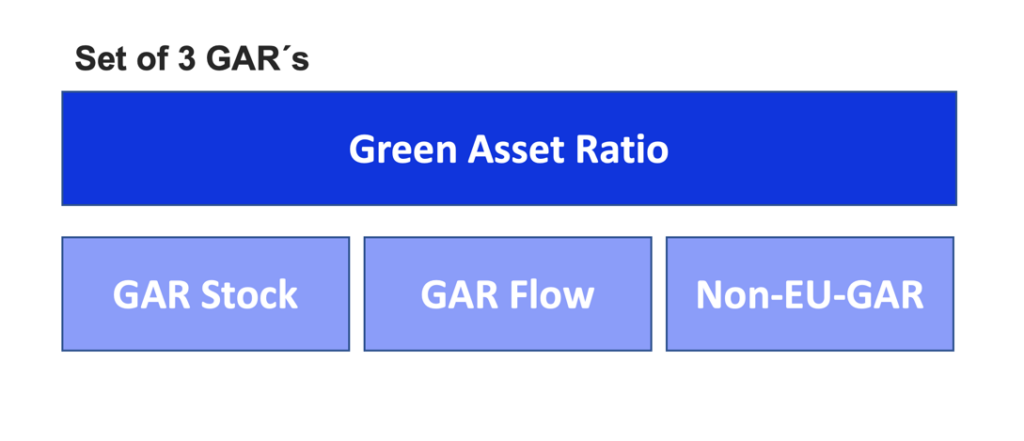

The GAR is not a stand-alone ratio. Rather, it is a set of three GARs – the “GAR Stock”, the “GAR Flow” and finally the “Non-EU GAR”. There are also four accompanying KPIs that provide information on the taxonomy compliance of the trading book, financial guarantees, assets under management and fee income generated by services other than lending and asset management.

The EBA identifies the GAR Stock indicator as the most important KPI. This indicator provides information on the taxonomy compliance of a bank’s assets as of a specific reporting date. This backward-looking information is to be complemented by the GAR flow indicator, which provides a more dynamic disclosure on green funding trends. Non-EU financing, on the other hand, is to be recorded under the non-EU GAR. Compliance with the latter indicator can be done on a “best-effort” basis. In addition, banks are expected to disclose their forward-looking objectives and strategy in relation to climate risk. This is to provide information on how banks are managing climate change-related transition risks and opportunities.

On 21 May 2021, the EBA published a GAR estimate of around seven to eight per cent for EU medium to large corporate exposures across a sample of 26 large banks (EBA/2021/Rep/11). These low GARs are no surprise. Due to the taxonomy, low GARs are still to be expected initially. Most of the companies and real estates for which banks provide financing are not yet compliant with the EU taxonomy. The draft delegated regulation on the implementation of GARs presented by the Commission in May 2021 could even result in initial ratios that are still below the EBA’s estimates. These estimates assumed that the green classification of a relatively small proportion of banks’ exposures of a limited subset of taxonomy-eligible assets would be in line with its own GAR proposals of February 2021. In contrast, the Commission proposes to match taxonomy-compliant assets with a broader range of exposures. As expected, this would result in a drop in ratios. Under the draft regulation, derivatives, trading book securities, interbank loans and loans to industries not covered by the EU taxonomy must be included in the denominator of the GAR calculation. This would lead to lower ratios for banks whose activities are less covered by the EU taxonomy (as capital markets business).

2. GAR and internal risk management

In the past, when bank supervisors tested newly developed supervisory initiatives in pre-studies, it has always turned out that the associated and legally binding requirement to do so did not take long. This applies especially to supervisory indicators and ratios. With the development of the GAR and the first corresponding disclosure exercises, the banking sector could face the same here.

As things stand, the GAR is (still) in its infancy. In the long run, however, it remains to be seen in what form the ratio will find its way into European banking supervision law. Is the GAR an exercise that will be discarded because financial markets players are not (yet) ready for the determination, analysis & control of the indicator? Could the GAR become mandatory “exclusively” in the form of disclosure requirements? Or will the GAR also have an impact on the capital adequacy of assets in the future? The answers to these questions will primarily have major implications for the bank´s risk managers “of tomorrow”.

It is already clear today that overall bank management is changing significantly. In times of pressure on earnings and margins, it is more essential than ever to understand revenue and cost drivers in detail in order to be able to take the right next steps from a strategic and operational perspective. Obviously, bank supervisors have recognised the need to acknowledge “green” activities of the financial sector as an important driver of the future with an impact on revenues and costs.

A closer look at the initiatives that regulators have developed, published and tested in a very short period of time under the guise of “ESG” leads to one central conclusion in this context: in the long run, the banking industry will have to integrate the topic of “green activities” not only in its marketing strategy, but also in its overall risk management. The revised CRR/CRD package contains a mandate addressed to the EBA (Art. 98; point 8 of the CRD), on the basis of which the European supervisory authority is mandated to develop appropriate criteria as well as stress testing processes and scenarios to be applied by banking institutions for the purpose of assessing the impact of ESG risks. This includes the assessment of the impact of adverse environmental developments on the financial position. Furthermore, the methods should also include quantitative and qualitative risk control mechanisms that are expected to be used in bank control and risk management. The relevance of the GAR for bank management should be obvious at this point at the latest.

Further evidence that bank supervisors are paying a great deal of attention to the topic of “green” activities is provided by the initiation of so-called “pilot exercises” at an early stage. The focus of these pilot exercises is to test the banks’ ability to identify, classify, evaluate and efficiently manage their own portfolios using the EU taxonomy. Furthermore, the exercises aim to determine how existing and newly developed approaches/tools for the classification of climate risks are performing and to what extent the institutions are already in a position to sufficiently identify and manage indicators such as the GAR and to master the challenges in connection with “taxonomy-compliant” data requirements.

While this is currently still a supervisory exercise under the direction of the supervisory authorities, it could become a binding regulation in three to five years, which is how long it takes to implement a new regulatory requirement. Against this background, it is even more important to use the insights gained from the “pilot exercises” to support the transition efforts of the banks. The transition aims at the willingness to invest in companies that are not yet sustainable and to actively support them on their way to sustainability. Besides the taxonomy-compliant data requirements, this is sometimes one of the most significant challenges.

When the integration of GAR into the overall risk management becomes mandatory, banks are encouraged to deal with the challenges at an early stage. The establishment of an internal GAR culture and infrastructure is indispensable for efficient GAR management. To this end, a process-related reorganisation is necessary in some areas. Above all, the data requirements and information needed to determine GAR are new in nature and need to be analysed and connected. As expected, there will be data and information bottlenecks for some activities and counterparties. For example, when classification according to taxonomy requirements is not possible. In these cases, solutions are needed that can be used to fill data gaps, e.g. through “data sourcing” or “proxies”.

An intensive examination of the “mechanics” of the ratio represents another essential field of action, as the GAR may have to be evaluated within the framework of risk-bearing capacity (ICAAP or ILAAP). Furthermore, early consideration of the functioning of the ratio is indispensable when it comes to modelling adverse scenarios and simulations, which are also an integral part of the normative perspective. However, stress tests and modelling can only be developed meaningfully if risk managers and bank controllers have a sufficient picture of which parameters affect the ratio and in what form (positive/negative). Thus, it will also be essential for the market units to understand which of their activities and counterparties trigger a “good degree of green” for the ratio and which do not, or to what extent the earmarking of financing can trigger an influence on the amount of the ratio.

3. GAR and implications in the context of market discipline

Fundamentally, the concept of market discipline within the banking sector stems from Pillar III of the regulations developed by the Basel Committee on Banking Supervision. Primarily, the market discipline regulation requires banks to disclose predefined prudential information and ratios, especially on regulatory capital. This is intended to provide market participants with a comprehensive insight into the risk exposure as well as the capital base of an individual bank in order to strengthen self-regulatory market forces. The banking sector will thus be “disciplined” through the requirements by market participants to provide information that is conducive to day-to-day business with investors or other stakeholders.

What this means in concrete terms for the disclosure of the GAR, in its role as a central “green” indicator developed by the EBA, and what the supervisory authorities see as the timetable for mandatory disclosure, is explained in more detail below.

Initial voices from banking experts assume that the disclosure of a GAR could increase, especially for capital market-oriented banks. Market observations make it clear that the zeitgeist of potential clients, capital providers and other stakeholders has shifted drastically in the direction of sustainable and ecological claims. Furthermore, the banking sector is subject to implementation pressure in terms of policy and regulatory initiatives on these issues. GARs are expected to contribute to the preference for “greener” financing over “brown” financing in the future. There is also a risk that institutions will come under refinancing pressure if investors with high sustainability requirements withdraw deposits from banks that report too low ratios. In this context, there is also a potential interaction with the SFDR, for example.

Since March 2021, the SFDR obliges all investment managers to declare/disclose whether their funds/products promote environmental or social characteristics (so-called Art. 8 funds) and whether their funds/products target sustainable investments (so-called Art. 9 funds). In turn, the SFDR is expected to lead to a surge in demand from asset managers for investments that meet sustainable criteria. In this respect, GARs and SFDRs could complement each other. For example, it is conceivable that the debt instruments of banks will be excluded or included in ESG-labelled funds. This creates a direct link to reputational risk.

In connection with the GAR disclosure under banking supervision law, the first fields of action are already foreseeable: the EBA envisages in principle that the GAR will not only be disclosed in the sense of quantitative quota values, but that qualitative information on the indicator will also be published, which should benefit the overall understanding of the markets: –

The final rules, announced by the European Commission on 6 July, are due to come into force in 2022. Banks will be required to make limited disclosures in 2022. The full set of KPIs will not have to be disclosed until 2024. The timetable is tight. Banks need the time to integrate the taxonomy-compliant information they require from large listed companies. These will not start publishing this information until early 2022 under the EU’s Non-Financial Reporting Directive (NFRD). Only such information published by NFRD companies will be included in the numerator of the GAR when it is introduced. Loans that do not fall within the scope of the NFRD – such as SME loans – are not part of the GAR.

Information on exposures to non-NFRD entities that publish the required data for GARs will be integrated from 2025, subject to EU Commission approval. Banks will not be required to publish KPIs that take into account their trading books or commissions and fees for commercial services other than the provision of financing until 2026.

Furthermore, in order to comply with the EBA’s disclosure proposals, institutions must first collect detailed information on their loan and securities portfolios in order to be able to harmonise balance sheet items with the classification requirements of the EU taxonomy.

Subsequently, there will be a need for reassessments – especially for those companies with high greenhouse gas emissions – and disclose them accordingly.

When the EBA prepared its report (EBA/2021/Rep/03), the supervisory authority prepared in parallel the draft ITS on ESG risk disclosure in the sense of Article 449a CRR. According to the EBA, the parallel development of both documents was considered necessary to ensure consistency in definitions and methodologies. If GAR disclosure requirements were to be included in the ESG Pillar III – ITS in accordance with Art. 8 of the EU Taxonomy, this would have certain implications. Firstly, the templates would have to fully comply with the information required under Art. 8 and furthermore, the GAR information should only be provided when the delegated act on the taxonomy for financial undertakings becomes applicable. Furthermore, in this case, the transition periods to be determined by the EBA in the context of the draft ITS would have to be aligned for certain groups of risk exposures, in particular those of non-financial undertakings.

4. Outlook

Following EBA’s recommendation, banks should already prepare for the GAR disclosure requirements. The results from the first supervisory bank surveys on the biggest impacts in connection with the implementation of the GAR further confirm this. The EBA asked a selection of banks and associations where they expected the biggest cost drivers of the implementation. Seven out of a total of ten large banks from five jurisdictions took part in the survey. According to the survey, the most significant cost drivers are seen in the following fields of action:

Nevertheless, the European Banking Authority also received feedback from the banks surveyed that initial attempts had been made to actively integrate sustainability aspects into business models (e.g. through multi-year business transformation initiatives, participation in supervisory impact studies such as those conducted by the EBA, or also partly through in-house developed methods for measuring climate risks). Although at a very early stage, only one of the banks reports that a KPI has already been implemented, which in parts follows the requirements of the EU taxonomy. In addition, initial staff training on sustainability issues and the integration of these into the “Client Relationship Management” (CRM) are said to have taken place. The EBA received feedback from the smaller banking institutions that the processes for integrating ESG issues into the strategy or risk management have not yet started.

The process of integrating climate risks into financial stability supervision has started. Quantifying the potential impact of climate risks on the banking sector has become a priority for regulators. This is reflected not only in the GAR, which has received particular attention through initial disclosure testing, but also in the taxonomy to which the GARs refer. In any case, the GAR is to be welcomed, because the ratio illuminates a previously unconsidered area in a standardised and comparable manner. However, it still seems too early to assess whether the ratio can contribute to making environmental data on loans and investments of EU banks comparable. It is important here that banks do not “greenwash” their relevant balance sheet items for the determination, measurement and reporting of the GAR in order to achieve better results. Against this background, the EBA plans to supervise the first disclosure according to taxonomy classification and, if necessary, to sharpen existing requirements based on these observations. Here is where banks are encouraged to participate in supervisory driven pilot test exercises since this will give them a competitive advantage and will help to influence the final outcome.

As long as the comparability is not yet given, it also remains to be seen to what extent stakeholders are convinced of the quality of the GAR and include it in their decisions. The estimates made so far by institutions and the first attempts to determine the GAR show that there are significant differences in the ratios. Both regulators and the banking sector have a lot of work ahead of them. The development of a uniform playing field as well as uniform data definitions and methods are essential here. Furthermore, the first critical voices are currently discussing that the GAR could possibly have disadvantages for the European banking market if the foreign banking sector refrains from introducing similar requirements.

Further reading:

Further development of the ESG risk framework is one of the EBA’s priorities for the coming year. Here is an excerpt:

HP1 2022 – ESG: provide tools to measure and manage risks

The EBA will monitor the effective implementation of ESG disclosure standards in 2022 of key ESG metrics, such as the Green Asset ratio and gradually expand the scope of disclosure reflecting the development of the EU taxonomy and data availability.

Following the publication of the EBA report on ESG risk management and supervision, and the technical standards for ESG disclosure, the EBA will continue investigating these risks, to inform risk assessment and policy making, and ultimately incorporate ESG risks into the risk management and supervision part of the Single Rulebook. As advised by the ACP, the EBA will pay particular attention to the specificities of SNCIs during this process to ensure proportionality is maintained.

The EBA will implement ESG considerations into its policy development via ESG impact assessments and will progress in incorporating ESG risks into its risk analysis and stress testing. The EBA will prepare a report for consultation on a potential prudential treatment of assets associated with environmental and/or social objectives. The EBA will also continue to participate in global, European and national initiatives in this regard, such as the Platform on Sustainable Finance and Network for Greening the Financial System also as strongly encouraged by the EBA’s ACP.

Following the Renewed Sustainable Finance Strategy of the Commission (expected to be published in 2021), the EBA envisages additional mandates to incorporate sustainability into financial services and improve ESG risk management. Based on the Commission’s consultation on the Renewed Sustainable Finance Strategy, areas where potential mandates might be directed to the EBA include green securitisation, green bonds, ESG risk management tools and ESG reporting standards.

https://www.eba.europa.eu/sites/default/documents/files/document_library/About%20Us/Work%20Pro gramme/2022/1021339/EBA%202022%20Annual%20Work%20Programme.pdf

[1] In its most recent report, the EBA called for ten-year plans for dealing with climate risks to be drawn up: Management and Supervision of ESG Risks for Credit Institutions and Investment Firms (EBA/2021/Rep/18).

Contacts

FANOS ADAMS

Manager

Fanos.Adams@L-P-A.com

Fanos Adams has over 7 years of consulting experience. She combines risk management expertise with a distinct Capital Markets focus and a profound knowledge of the European banking domain & supervisory initiatives and regulations.

HANS JOACHIM LEFELD

ESG Consulting Partner

Hans.Joachim.Lefeld@L-P-A.com

Hans Joachim Lefeld is Partner in LPA´s Frankfurt-based consulting team. He has over 20 years of end2end regulatory reporting expertise and is LPA´s responsible ESG Consulting Partner.

CHRISTIAN BEHM

Partner

Christian.Behm@L-P-A.com

Christian Behm is partner in LPA´s Frankfurt-based risk consulting team. He has over 15 years of experience in executing regulatory required risk assessments under the so-called supervisory normative risk perspective.

NICKY MARCO HEBER

ESG Campaign Lead

Nicky.Heber@L-P-A.com

Nicky Heber has over 10 years of consulting experience in the European Capital Markets sector, ranging from banks to clearing houses and asset managers. He is LPA´s ESG campaign lead for our international banking clients and partners.

Manager Consulting , Germany

Fanos Adams has over 7 years of consulting experience. She combines her experience in implementing supervisory driven initiatives with a distinct Capital Markets focus and a profound knowledge of the European banking domain.

Partner, Germany

Partner, Germany

Director, Germany

Nicky Heber has over 10 years of consulting experience in the European Capital Markets sector, ranging from banks to clearing houses and asset managers. He is SME for implementing European regulatory requirements in the context of ESG.

Written by Sandro Schmid

8 Mar, 2024

Written by Sophia Pfannes

21 Dec, 2023

Written by Sahak Artazyan

21 Dec, 2023

Written by Gonzalo Plana

21 Dec, 2023

Written by Charles Kim-Régnier

21 Dec, 2023

Written by Julie Bradini

21 Dec, 2023