Consulting | IBOR | Regulatory

Written by Christian Behm

Apr 26, 2022

Management of CSA portfolios is a crucial aspect of a successful IBOR transition program. CSAs with EUR or USD-cash collateral need to be amended in the upcoming months to reflect the transition to new RFRs. This is the right time to review existing derivative portfolios and optimize counterparty structures and collateralization. Timely quantification is essential to perceive the potentially high valuation effects and to avoid any losses during the transition.

Introduction

The IBOR transition brings many changes to the capital markets sector. One of the critical challenges of transition management is the amendment of collateralization for OTC derivatives. PAI (and implicitly discounting) needs to be adapted for EUR and USD-cash collateral from EONIA and EFFR to the new Risk Free Rates (RFRs) €STR and SOFR. This has to be done by the end of 20211 (EUR) and the end of 20202 (USD), respectively. While the adjustment for cleared derivatives is managed centrally by the CCPs, counterparties of bilaterally collateralized derivative portfolios must amend the collateral agreements by themselves. This requires EONIA or EFFR based legacy CSAs to be negotiated and compensation payments between counterparties to be settled. Complexity is increased further as many market participants still have some non-standardized legacy CSAs with features such as embedded floors or thresholds in place. Strategic options (backloading, counterparty selection, novation) should be analyzed and executed, if beneficial.

Pricing of derivatives

While derivatives with end customers are mostly uncollateralized, trading between financial institutions usually happens on a collateralized basis. In clearing, the collateral terms and conditions are managed centrally by the CCP. Collateral is posted daily, balancing the change in market value (variation margin) to ensure that the trade is fully secured. The posted collateral receives interest based on an overnight rate. The same overnight rate is used within the valuation process to discount the future cash flows, so that the collateral plus interest equals the future cash flows in a forward scenario. This is risk-neutral pricing. For bilateral trades the collateral terms and conditions are negotiated individually using a Credit Support Annex (CSA). The collateralization of bilateral trades can be far from perfect (in comparison to cleared trades), especially for non-standardized CSAs. This leads to counterparty risk, funding costs and capital costs which are addressed by separate valuation adjustments – the so called xVAs.

CSA Management

Generally, the question arises how to reflect the upcoming changes of reference rates in CSAs and how to proceed regarding the resulting valuation shift. The portfolio view of CSAs requires a dedicated management of the transition to avoid any unnecessary losses during this process. Active management and optimization of the CSA transition into the new world can exploit hidden value potential.

Given the fact that all existing CSAs with EUR- or USD cash collateral need to be amended during the upcoming months, the question arises how to prepare and define the optimal strategy to tackle the transition. Dependent on the individual situation, this could mean avoiding value losses, reduction of capital, standardizing contracts or minimizing processual risks.

Backloading

The most obvious amongst the mentioned options is backloading of the portfolio to a CCP in order to reduce uncertainties in the process and enforceability by following a centrally managed transition procedure. While the discounting switch for EUR derivatives from EONIA to €STR by LCH and EUREX has already been implemented, the switch for USD derivatives from EFFR to SOFR is planned for 19 October, 2020. Given this timeline, a backloading of USD derivatives can still participate in a centrally executed transition procedure. Independent of the transition clearing offers further advantages such as reduced capital requirements. Accordingly, backloading opportunities should be analysed in the context of the CSA transition. Despite the advantages to do so, backloading to a CCP must be funded, as it may entail additional liquidity requirements due to the posting of initial margin. Furthermore, there might be non-clearable transactions in the portfolio, leaving a residual portfolio to be assessed and managed separately. Depending on the structure of the residual portfolio, backloading might increase the residual exposure and hence leads to additional xVA effects. Additional efforts depend on the current onboarding status to a CCP.

Standardization

Many institutions deal with some portion of non-standardized CSAs not reflecting the newest market standards (e.g. floors on collateral interest or large thresholds/ MTAs). In these cases, the shift to new reference rates causes further complexities. It might be reasonable to standardize the contracts while transitioning to the new RFRs. Standardized CSAs minimize or cancel out the influence of xVAs and facilitate the management of existing derivative portfolios and the closing of new trades.

Valuation

A revaluation is necessary for all CSAs. For non-standardized CSAs there is the need to deal with (partially) uncollateralized derivatives. This results in a more complex calculation where xVAs for counterparty risk, funding costs and capital costs need to be taken into account. Valuation effects are counterparty specific and depend strongly on xVA methodology as well as the portfolio structure, which leads to complicate negotiations. A detailed example on the valuation effects is illustrated in the case study below.

Institutions should timely define an action plan and make the technical preparations to be able to quantify the valuation and xVA effects of the RFR-transition to engage in bilateral negotiations. It takes a thorough preparation and strategy to avoid common pitfalls and to take advantage of optimization potential. Operationalization of the amendment is especially a challenge for large CSA portfolios.

Summary

For the amendment of fully collateralized derivative portfolios to the new RFRs, both counterparts have to agree upon a compensation payment driven by the changed discounting rate. For standardized CSAs, the valuation effects could be calculated as the difference between the net present values (NPVs) – using the current OIS rate (EONIA/EFFR) and the new RFR (€STR/SOFR) as discount rate. For non-standardized CSAs, xVAs have to be taken into account which are distributed asymmetrically between the counterparts, determining the need to negotiate the compensation payment.

The forthcoming tasks for the transition include clustering of CSAs, prioritization of actions, selective pre-wiring with counterparts and the timing of the transition. After quantification of valuation effects, the negotiation with counterparties needs to take place.

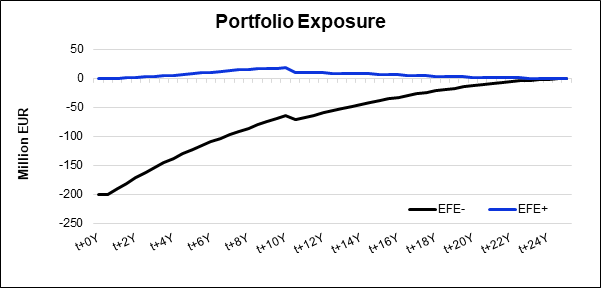

Case-Study (EONIA-€STR transition)

In the following, valuation and xVA effects are examplified based on a model portfolio. The notional of the portfolio is EUR 1bn. It consists of three different swap types:

| Swap Type | Currency | Notional | Maturity | Amortization Schedule | At-market NPV |

|---|---|---|---|---|---|

| Payer Swap | EUR | EUR 0.7bn | 25 | Amortizing to 0 | EUR -175m/ -25% |

| Payer Swap | USD | EUR 0.1bn | 25 | Amortizing to 0 | EUR -25m/ -25% |

| Cross-Currency Swap | EUR/ USD | EUR 0.2bn | 10 | Bullet/ Exchange of notional | EUR 0m/ 0% |

| Total | EUR 1bn | EUR -200m |

The high negative market value results in a correspondingly asymmetrical exposure profile. The exposure simulation and the results shown in this case study are based on calculations from our pricing engine LPACalc3.

For the consideration of the xVAs, an economical perspective is incorporated instead of an accounting perspective. Hence, no DVA is recognized. FVA will be presented incl. ColVA and without MVA.

Two collateralization scenarios are examined:

The results are presented for both counterparties (Cpty A & Cpty B). Unless explicitly stated otherwise, the results are interpreted from the viewpoint of Cpty A.

| Scenario 1: Collateral interest: EONIA, min 0% Threshold: EUR 0 | Scenario 2: Collateral interest: EONIA Threshold: EUR 20m | |||

| View | Cpty A | Cpty B | Cpty A | Cpty B |

| CVA | EUR 0.0m | EUR 0.0m | EUR -0.5m | EUR -4.3m |

| FVA | EUR 9.1m | EUR -9.1m | EUR 3.0m | EUR -2.4m |

| KVA | EUR -2.5m | EUR -4.2m | EUR -3.1m | EUR -10.9m |

Since we assume a perfectly collateralized and hedged portfolio in scenario 1, there is no CVA. In scenario 2, a threshold leads to counterparty risk. Since no DVA is incorporated, CVA is negative although the portfolio has a strongly negative NPV.

The FVA in scenario 1 is the result of not paying interest (receiving negative interest) on the collateral posted due to the EONIA floor. This positive effect is weaker in scenario 2, since interest is payed (receiving negative interest) for collateral, but not for the threshold of EUR 20m.

Despite full collateralization, there is also a significant KVA for scenario 1. The underlying capital requirement results from the PFE component (exposure method) and CVA Risk Capital Charge. The KVA in scenario 2 is larger in comparison to scenario 1 because of the uncollateralized value due to the threshold.

Switching the discounting and the price aligned interest from EONIA to €STR, the following effects would be observed:

| ∆ NPV | ∆ xVA | Net Effect | Net Effect incl. Standardization | |

| Scenario 1 (Cpty B) | EUR -1.3m (EUR +1.3m) | EUR +1.1m (EUR -1.1m) | EUR -0.2m (EUR +0.2m) | EUR -10.4m (EUR +10.4m) |

| Scenario 2 (Cpty B) | EUR -1.3m (EUR +1.3m) | EUR +0.2m (EUR -0.3m) | EUR -1.1m (EUR +1.0m) | EUR -3.2m (EUR +14.7m) |

In both scenarios, there would be a negative NPV effect, resulting in a compensation payment from counterparty B. In both scenarios the NPV effect would be partially offset by a contrary xVA effect. The economic effect of the conversion is therefore smaller than the pure NPV effect indicates. In case the counterparties want to standardize the CSA, the compensation payment needs to incorporate the full xVAs – the resulting economic effect is represented by the “Net Effect incl. Standardization” in the table above. Due to the asymmetric xVAs the resulting net effects incl. standardization are different for the both counterparties, opening a win-win-corridor for negotiations.

From the outcome of the case study one can see that the valuation effects can be significant. Institutions should not underestimate the valuation effects to avoid losses during the transition. The effects depend largely on the structure of the portfolio and the collateral conditions. In particular, deviations from standardized CSAs (EONIA floor and thresholds) may lead to higher economical effects than the delta of the NPVs would indicate and complicated negotiations. Therefore, a detailed analysis for the CSA portfolio is required.

CSAs need to be amended in the coming months to reflect new RFRs. Depending on the CSA, this might be a challenging task in terms of quantification. The need to manage the transition on a portfolio level is important. For that reason, an initial (quantitative) analysis of the status quo should be done. The transition strategy should deal with the following aspects:

Amending CSAs is a crucial part for a successful IBOR transition, unlocking hidden value and minimizing potential losses, if done the right way.

Partner, Germany

Manager Consulting , Germany

Written by Sandro Schmid

8 Mar, 2024

Written by Sophia Pfannes

21 Dec, 2023

Written by Sahak Artazyan

21 Dec, 2023

Written by Gonzalo Plana

21 Dec, 2023

Written by Charles Kim-Régnier

21 Dec, 2023

Written by Julie Bradini

21 Dec, 2023